WEEKLY MARKET SUMMARY

Global Equities: Stocks advanced in weekly trading, driven by continued strength in corporate earnings despite continued geopolitical uncertainty. The S&P 500 added 0.9% during the week and the Nasdaq Composite gained 1.1% as mega cap tech earnings provided a boost. The Dow Jones Industrial Average advanced 0.5% on the week, but the gains were largely attributable to a blowout quarter from Caterpillar (CAT). US small cap stocks continued to shine, tacking on another 0.9% and propelling the Russell 2000’s year-to-date total return to over 13%. Developed market international stocks gained just 0.3%, constrained by headwinds from lower projected Japanese growth and increasing strain on European markets due to higher energy costs, while emerging market stocks advanced 0.6%.

Fixed Income: The 10-year Treasury yield ticked higher to end the week at 4.37% as inflation accelerated and the dissent grew at the Fed over the future path of interest rates. The Fed elected to hold rates steady as widely anticipated during Jerome Powell’s final meeting as Fed Chair, with some members wanting to remove language implying a bias towards future cuts. In his final press conference, Powell stated he would be staying on as a Fed member, citing the unprecedented political pressure that has been exerted on the Fed to cut rates.

Commodities: Oil prices were higher during the week, with Brent Crude briefly exceeding $126 per barrel and US benchmark West Texas Intermediate (WTI) surpassing the $110 level as negotiations between the US and Iran have reached an impasse and rumors of further US strikes on Iranian energy infrastructure surfaced. The United Arab Emirates announced it will no longer participate in OPEC, weakening the cartel and potentially introducing more supply into the market. US consumers are feeling the pain at the pump, with the national average gasoline price hitting $4.39, just 12% below the all-time record of $5.02 in 2022.

WEEKLY ECONOMIC SUMMARY

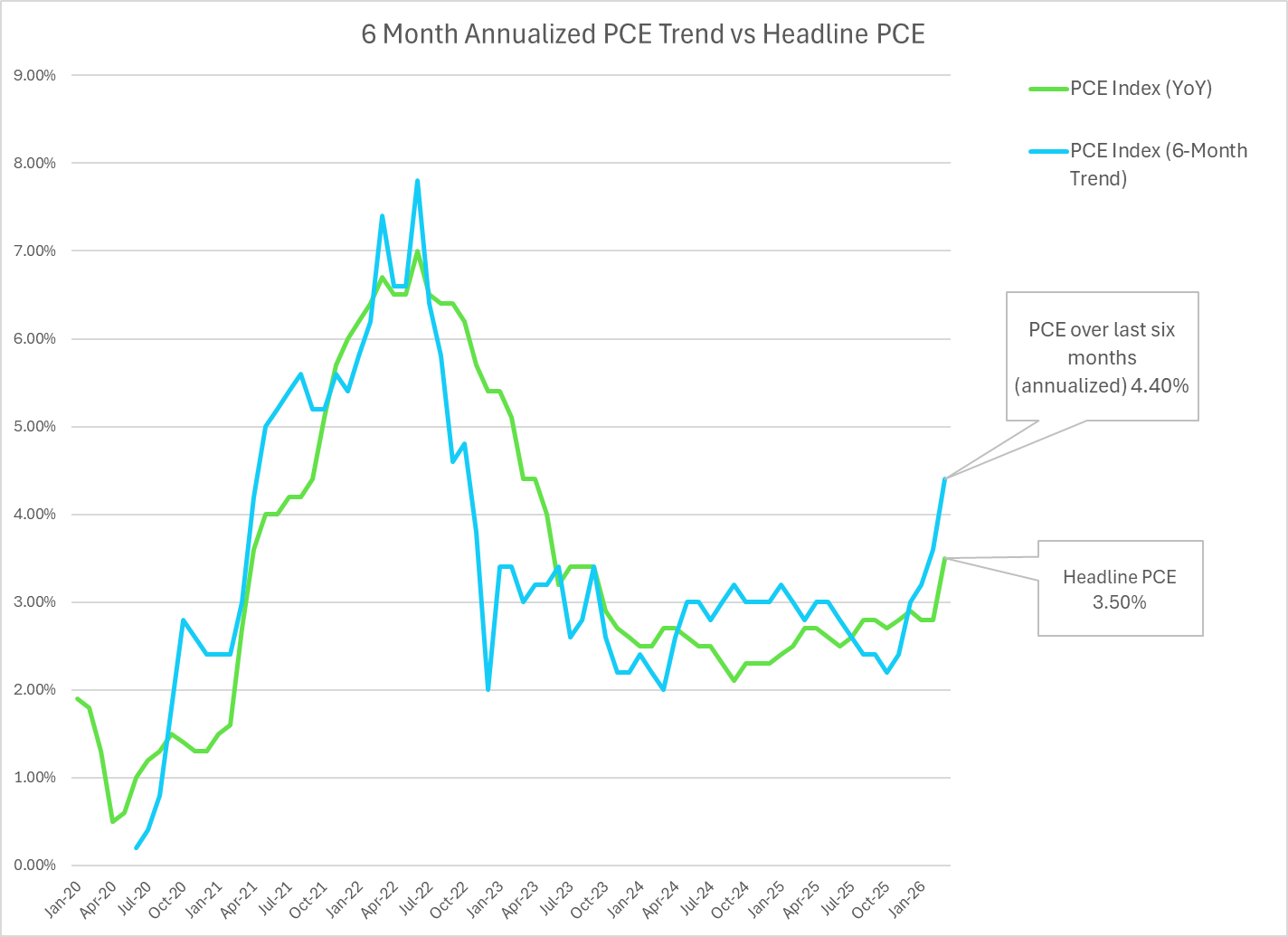

Energy Shock hits Inflation: The Personal Consumption Expenditures (PCE) price index advanced 0.7% in March to an annual rate of 3.5%, driven by an 11.6% spike in Energy Goods and Services, which included a 20.9% monthly surge in gasoline prices. The Fed’s preferred inflation measure, Core PCE (excluding food and energy), gained 0.3% during the month to reach an annual rate of 3.2%. With the Fed targeting 2% annual inflation, rate cuts remain off the table for the foreseeable future and several Fed officials argued that policy language should be altered to account for the growing possibility of a rate hike.

GDP Stable: The initial reading of first quarter Gross Domestic Product (GDP) was slightly below economists’ consensus at 2.0% vs the estimated 2.1%, but well above the Atlanta Fed’s forecast of 1.2%. The biggest driver of growth was the AI buildout, which accounted for three-fourths of the total GDP growth. Government spending also rebounded sharply after the recent shutdowns and spending on the Iran war also contributed to the increase. Detractors to growth included a surge in net imports after tariffs were struck down, along with lower discretionary consumer spending.

Earnings Season: Five of the “Mag 7” stocks reported this week, with mixed results. The biggest winner was Alphabet (GOOG), driven by 20.6% revenue growth and 63% cloud revenue growth. Shares of Alphabet surged 10% in response to the strong quarter. Apple results also impressed investors, with strong China sales and a new $100 billion stock buyback giving shares a modest post-earnings boost. Investors sold shares of Amazon (AMZN) and Microsoft (MSFT) despite top- and bottom-line beats from both tech giants. Meta (META) was the biggest loser as investors grew skeptical that the $125-$145 billion in planned capex will pay off. Unlike its peers, Meta does not offer a cloud business to rent out computing power to other companies and is instead leveraging its AI investment to enhance advertising tools and drive engagement on its social media platforms.

The week ahead: Notable names on the weekly earnings docket include Palantir (PLTR), Advanced Micro Devices (AMD), Disney (DIS), Shopify (SHOP), and Novo Nordisk (NVO).

CHART OF THE DAY

The Chart of the Day shows the headline Personal Consumption Expenditure (PCE) inflation over the last twelve months (green line), compared to the annualized trend over the last six months (blue line). The Iran war energy shock has driven PCE inflation up to its highest level since May of 2023 and the six-month trend shows inflation rising at the fastest rate since October 2022. If the Strait of Hormuz is reopened, PCE should decelerate, but it may take several months for the effects of higher energy prices to work their way through the global economy.

Data from Bureau of Economic Analysis, chart and commentary by VestGen Investment Management.