WEEKLY MARKET SUMMARY

Global Equities: Optimism over ceasefire talks kept markets positive for a second consecutive week, marked by a 3.6% return for the S&P 500, the index’s strongest week since November. Technology was a standout leader, with semiconductor names hitting all-time highs even as software broadly remains under pressure on concerns about AI disruption to traditional SaaS business models. The Nasdaq Composite surged 4.7% and the Dow Jones Industrial Average advanced 3.0%. Small Caps ended the week up 4.0%, while foreign Developed Market stocks gained 4.3%. Emerging Markets were the standout performers, registering a weekly gain of 7.0% as the prospect of energy price relief propelled gains.

Fixed Income: Treasury yields were essentially unchanged on the week, with the 10-Year ending at 4.31% as the relief from the ceasefire announcement was offset by hot inflation data. Fed rate cut expectations remained subdued, with the probability of a cut at any 2026 FOMC meeting holding below 20% and market pricing pushing the first likely cut out to mid-2027. Private Credit stress continued to build, with Ares Management capping redemptions from its Strategic Income Fund at 5% after receiving $1.2 billion in redemption requests during the first quarter. Across the Private Credit sector, investors have attempted to redeem more than $20 billion in the first quarter, underscoring how quickly sentiment has shifted in a sector that saw explosive growth in recent years.

Commodities: Oil markets staged a dramatic reversal as US West Texas Intermediate fell from over $112 a barrel to under $96, with Brent Crude ending near parity. Despite the optimism, the Strait of Hormuz remained effectively closed to oil tanker traffic. US dollar weakness helped propel gold prices to a 2% gain, ending the week at $4,780 per ounce.

WEEKLY ECONOMIC SUMMARY

Energy Shock Hits CPI: The March Consumer Price Index showed inflation accelerating sharply, with prices rising 0.9% monthly and 3.3% annually, the highest reading since May 2024. The surge in energy prices was jaw-dropping, with Gasoline up 21.2% in the month and Fuel Oil 30.7% more expensive. In aggregate, the Energy category ended March 10.9% higher to bring the annual rate of Energy inflation up to 12.5%. Core CPI (excluding food and energy) was up more modestly, rising 0.2% in March to an annual rate of 2.6%.

Consumer Sentiment Dismal: The University of Michigan’s preliminary April consumer sentiment index dropped to 47.6 from 53.3 in March, reflecting mounting concern about energy-driven inflation, the ongoing Iran conflict, and its effects on household purchasing power. The reading was the lowest in the 79-year history of the survey, showing widespread pessimism across all age, income, and political demographics.

Iran Conflict: Week six of “Operation Epic Fury” ended on a hopeful note with ceasefire talks slated for the weekend, which prompted a rally in stocks. There was some skepticism that an agreement could be reached however, with Iran reportedly demanding that the US legitimize its sovereignty over the Strait of Hormuz, paying reparations for war damages, and fully retreating from the entire Middle East region, among other concessions. Those doubts proved correct, as Iran rejected the “best and final offer” from the US over the weekend. The US will now be implementing a naval blockade of the Strait of Hormuz while seeking to clear Iranian mines in the area, as the state of the ceasefire remains uncertain.

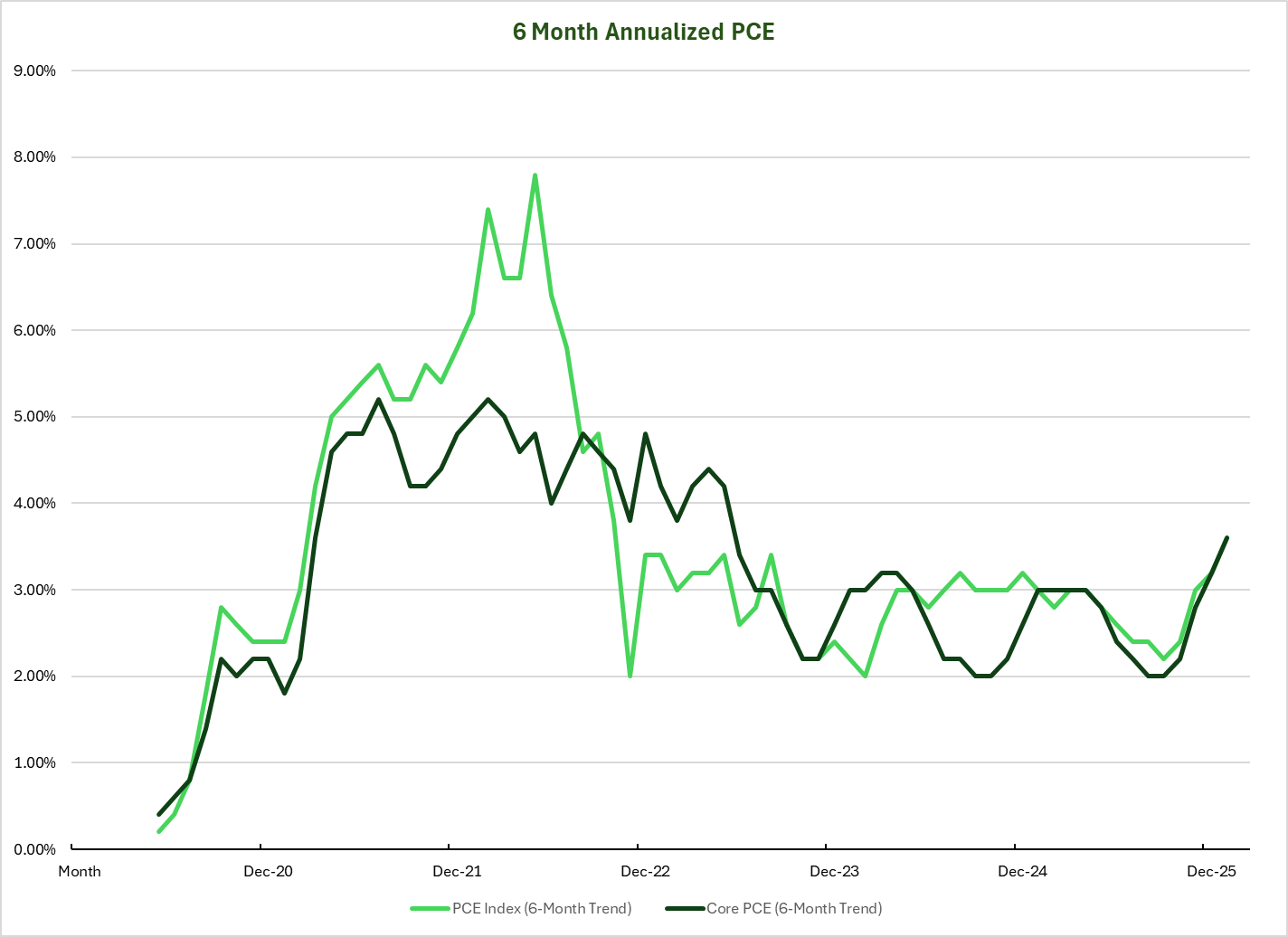

CHART OF THE DAY

The Chart of the Day shows the annualized rate of headline and Core Personal Consumption Expenditure (PCE) Index over the trailing six months, annualized. PCE is the Fed’s preferred measure of inflation, although it lags CPI by one month and the most recent dataset precedes the Iran conflict and associate spike in energy inflation. Even before the looming energy shock hits the PCE, the most recent half-year trend shows a breakout in inflation above the 2-3% range where it has been contained since 2023. The Cleveland Fed predicts that April inflation (PCE and CPI) will come in around 3.6% as the impact of higher energy prices works its way through the economy.

Source: US Bureau of Economic Analysis. Commentary by VestGen Investment Management.