WEEKLY MARKET SUMMARY

Global Equities: Stocks were hit with about of late-week volatility, resulting in a broad-based selloff that brought the nine-week streak of market gains to an abrupt end. The catalyst for the selloff was a case of “good news is bad news” in the form of a May jobs report that greatly exceeded estimates and led to a repricing of Fed interest rate expectations. The high-flying tech sector bore the brunt of the selling, sending the Nasdaq Composite -4.7% lower in its worst weekly performance since April 2025. The S&P 500 slipped -2.6% and the Dow Jones Industrial Average fell –0.2%. Small cap stocks pulled back on the prospect of higher interest rates, ending the week -3.0% lower. Heavy selling in semiconductor names crushed emerging market stocks, which fell -5.9%, while foreign developed markets ended -2.4% on dual headwinds from higher rates and a stronger dollar.

Fixed Income: The 10-Year Treasury yield edged higher after the jobs data, rising to 4.54%, while 30-year yields eclipsed 5%. Expectations for at least one 2026 rate hike ended the week significantly higher at 72%, with the market pricing in between 1 and 4 rate hikes on the table before the year is out.

Commodities: WTI crude oil futures jumped over 6% during the week after the situation in Iran deteriorated and hopes of a near-term resolution faded. US benchmark West Texas Intermediate ended the week above $93 and Brent Crude was trading around $96 by week’s end. The selloff in stocks extended to gold markets, which fell sharply on Friday to end the week with spot gold priced at roughly $4,365 per ounce.

WEEKLY ECONOMIC SUMMARY

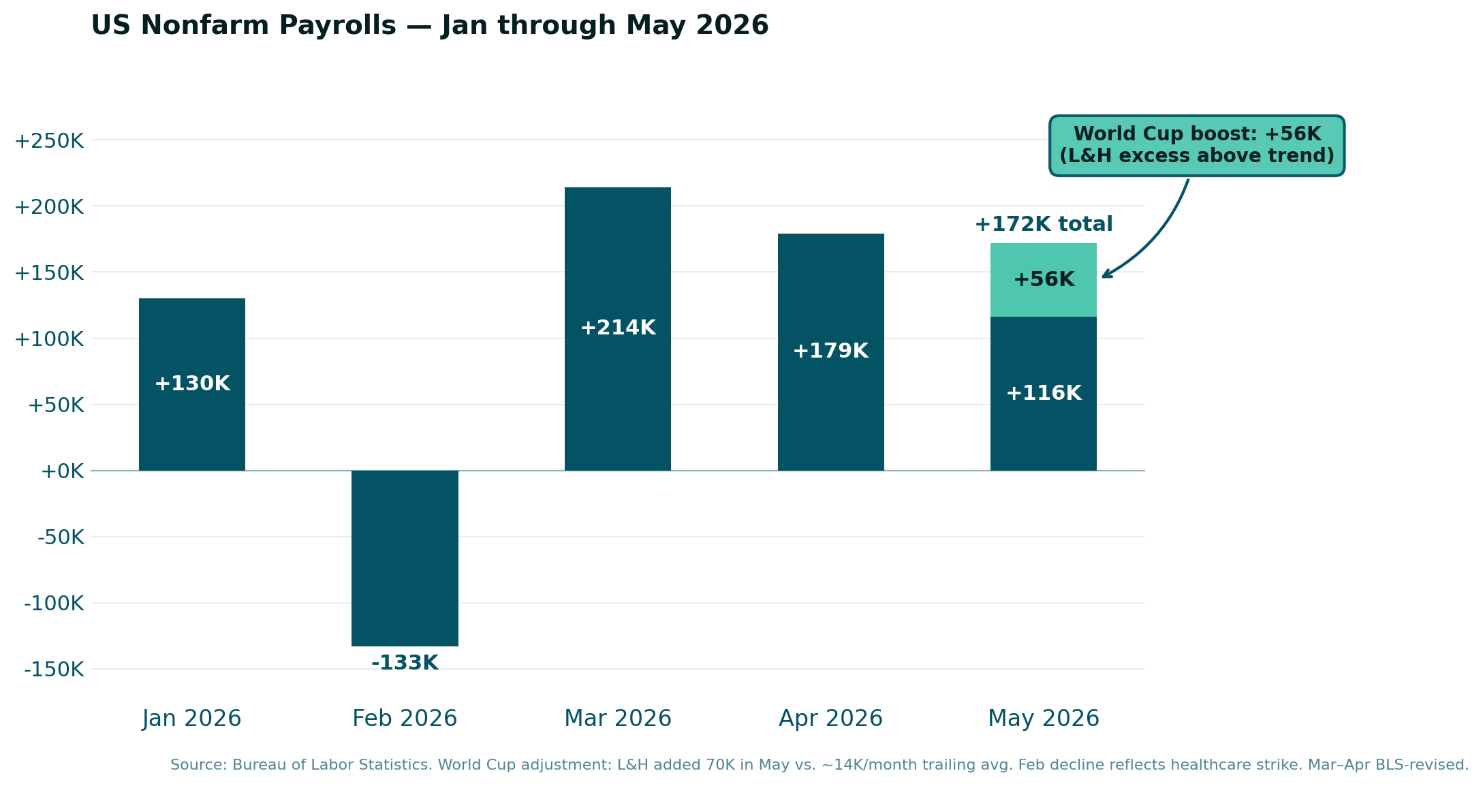

May Employment Report: The week’s dominant story was Friday’s nonfarm payrolls release, which delivered a significant upside surprise. The US economy added 172,000 jobs in May, more than double the 85,000 consensus forecast, while March and April payrolls were revised up by a combined 93,000 positions. Gains were concentrated in leisure and hospitality, attributable to temporary hiring in advance of the World Cup. The unemployment rate remained steady at 4.3%. The report effectively extinguished any remaining expectations for a Fed rate cut in 2026 and drove yields sharply higher across the curve.

Iran War Update: Diplomatic progress on a ceasefire framework remained elusive during the week. While President Trump said talks with Tehran were progressing well, Iran-backed Hezbollah rejected a US-brokered ceasefire proposal for Lebanon, a key sticking point given Israel’s continued military operations there. The breakdown in negotiations underscored that a resolution to the Strait of Hormuz disruption remains uncertain. While President Trump attempted to redefine “ceasefire” as meaning combatants are “shooting in a more moderate manner”, Iran escalated the conflict with a drone and missile strike on Kuwait International Airport that killed one and injured more than sixty other people, in addition to devastating damage to the building.

Earnings Season: Broadcom’s (AVGO) quarterly earnings report left AI-focused investors disappointed after the company left its full-year AI chip revenue targets unchanged, triggering a sharp selloff not only in Broadcom shares but across the entire semiconductor complex. The reaction was a stark contrast to the AI euphoria that had driven chip stocks to record highs in prior weeks and raised questions about whether the pace of AI infrastructure spending is plateauing at current levels.

The week ahead: A fresh batch of inflation data is due out with the Consumer Price index on June 10th and the Producer Price Index the following day. The Cleveland Fed forecasts CPI will reach 4.18% and Core CPI will come in at 2.82%.

CHART OF THE DAY

The Chart of the Day shows the year-to-date trend in hiring, which would typically be a welcome sign for the economy. Aside from a healthcare strike-impacted February jobs report, employment growth has been strong all year long, negating concerns that workers are being replaced by AI. The March – May 2026 three-month total of 565,000 is the strongest such stretch since the post-pandemic labor market recovery in 2021. The strong jobs numbers may be a bit misleading however, since many of the March gains and possibly some of April’s data can be attributed to a bounce-back rehiring of striking healthcare workers from February. May’s blowout data is still an impressive 116,000 after accounting for an estimated 56,000 temporary hospitality jobs created for the World Cup, but backing those workers out shows a declining trend over the last three months. Local government jobs also increased by an outsized 55,000 in May, which caused some economists to question the BLS data. Still, the recent six-figure jobs gains will give the Fed plenty to debate and presumably win more votes over to the hawks’ side.

Data: US Bureau of Labor Statistics.

Chart and commentary by VestGen Investment Management.