WEEKLY MARKET SUMMARY

Global Equities: Stocks posted their first weekly gain since the Iran conflict began amidst heightened volatility and a constantly shifting narrative surrounding the war. The S&P 500 ended the week up 3.4%, its first weekly advance since the conflict began five weeks ago, while the Nasdaq gained 4.4% and the Dow advanced 3.0%. Small caps gained 3.4% as falling Treasury yields late in the week eased pressure on rate-sensitive smaller companies. Foreign stocks also were positive during the week, with Developed Market equities up 4.5% and Emerging Markets up 2.5%.

Fixed Income: Treasury yields ended the week lower, with the 10-Year yield easing to 4.31% on hopes for a quicker resolution to the global energy supply disruption. Mortgage rates continued to grind higher as the average 30-year fixed-rate mortgage hit 6.46%, up 8 basis points from the prior week and roughly 50 basis points higher than just a month ago. Private credit concerns hit the headlines once again as Blue Owl Capital (OWL) reported record withdrawal requests from two of its investment vehicles, leading the firm to cap immediate payouts at 5% of outstanding shares. Investors were seeking to pull 41% of the outstanding shares of the $6.2 billion Blue Owl Technology Income fund and 22% of the $36 billion flagship Credit Income fund.

Commodities: Oil markets were predictably volatile amidst conflicting diplomatic signals, with Brent crude spiking above $111 a barrel early Thursday following an address to the nation by President Trump Wednesday evening. Word that Oman and Iran were working to establish a protocol for the Strait of Hormuz brought some relief to Brent prices. US West Texas Intermediate crude prices rose even more aggressively than Brent, leading to a structurally unusual inversion of the Brent-WTI spread as Brent ended the week at $109 and WTI hit $112 a barrel. Gold prices pulled back modestly, ending the week at roughly $4,600/oz.

WEEKLY ECONOMIC SUMMARY

March Jobs Report: Markets were closed for Good Friday, so there was no immediate reaction to the March Jobs report’s surprisingly strong 178,000 job gains, which crushed the consensus estimate of just 51,000. Government jobs were a net negative as private payroll gains totaled 186,000. February’s -92,000 job losses were revised further downward to -133,000, with private payrolls accounting for -129,000 of the revised totals. The unemployment rate also eased unexpectedly to 4.3%. Assuming no significant downward revisions, the strong jobs data should give Fed participants concerned about stagflation some optimism that economic growth can offset the pending energy-driven inflation.

Manufacturing Activity Improves: President Trump’s tariffs were intended to spur a shift to domestic manufacturing by discouraging imports, but manufacturing activity has thus far been anemic since Liberation Day. Manufacturing showed a rare spark of life in March, however, with two separate reports signaling the first real expansion in years. The ISM Manufacturing PMI climbed to 50.3, crossing the crucial 50-point threshold that separates growth from contraction for the first time in 16 months. This rebound was fueled by a surge in new orders and production, though thePrices Index also jumped to 55.8,indicating that rising energy and raw material costs are already hitting factory floors. A separate report, the S&P Global PMI, was also expansionary at 51.9, providing further evidence that a reindustrialization trend may finally be taking place.

Iran Conflict: The fifth week of “Operation Epic Fury” in Iran was marked by shifting narratives, with President Trump seemingly looking to wrap things up early in the week by declaring the objectives close to complete and stating he would leave without securing the Strait of Hormuz. Rumors that US ground forces would soon be involved preceded a Wednesday evening address to the nation, but Trump provided no confirmation of these reports and gave little insight into the timing of any withdrawal, adding to the confusion. The conflict appeared to be escalating heading into the weekend after US-Israeli strikes destroyed the B1 bridge in Karaj, Iran, the tallest bridge in the Middle East, killing 8 civilians and wounding another 95 according to Iranian state media. On Friday, Iranian forces shot down a US F-15E Strike Eagle, and there were unconfirmed reports that other search-and-rescue aircraft were also downed in Southern Iran.

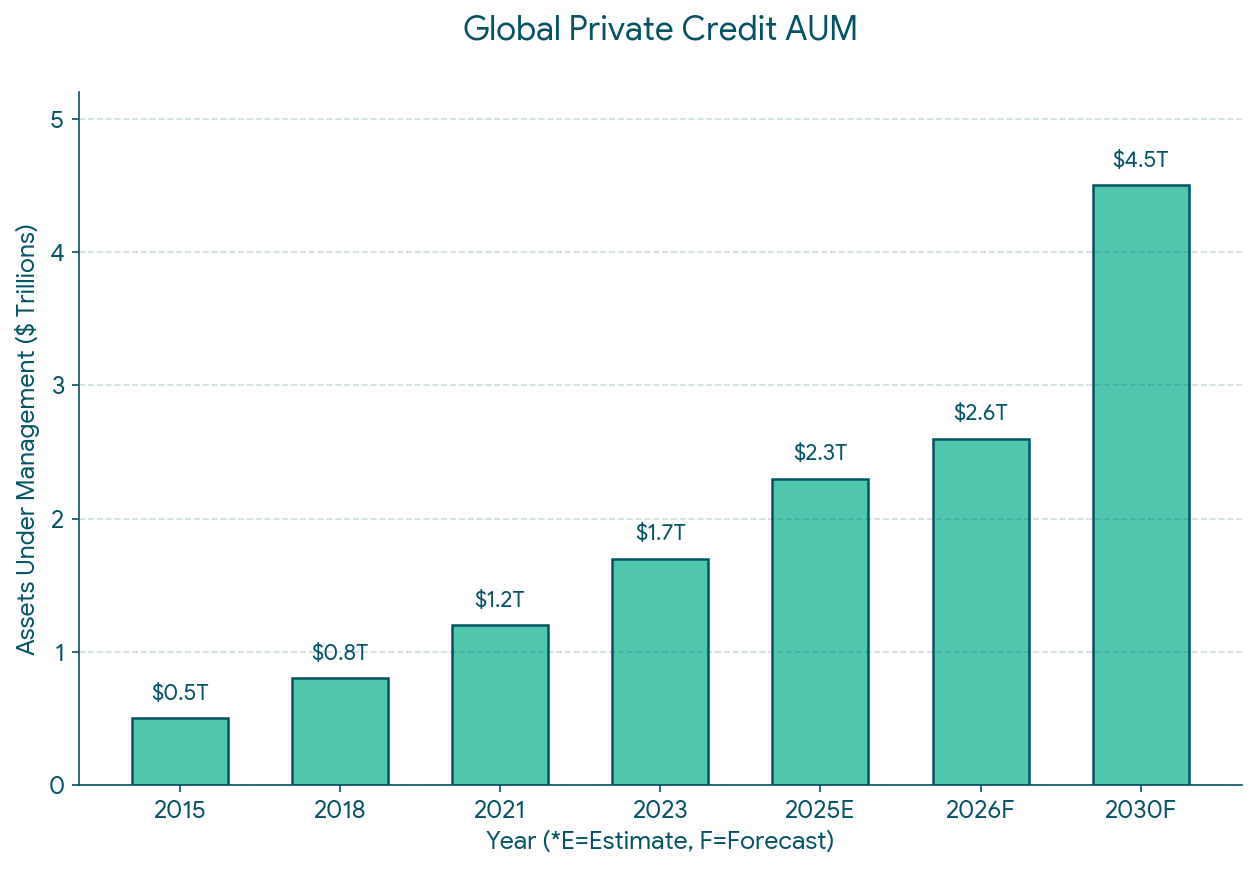

CHART OF THE DAY

The Chart of the Day shows past and projected growth in global Private Credit markets. On March 30th, the U.S. Department of Labor issued a proposed rule that would significantly ease the path for including private credit, private equity, and other alternative assets in 401(k) and 403(b) retirement plans. This move follows a 2025 executive order from the Trump administration aimed at “democratizing access” to high-yield alternative investments for ordinary savers. A 60-day public comment period is now underway, with the goal of finalizing the rule by year-end 2026. With recent headlines regarding redemption caps and investors seeking liquidity, it will be interesting to watch how plan sponsors receive this new asset class.

Source: Preqin. Commentary by VestGen Investment Management.