WEEKLY MARKET SUMMARY

Global Equities: Stocks staged a volatile but resilient recovery following the prior week’s steep selloff. Geopolitics were the driving force behind the rally as the Iran situation shifted dramatically from escalation to possible peace. The three major US large cap indices all posted weekly gains with the S&P 500, Nasdaq Composite, and Dow Jones Industrial Average all gaining 0.7%. US small cap stocks were strong outperformers, ending 4.0% higher. Foreign developed stocks rose 2.7%, while emerging markets led with a 5.1% weekly surge on hopes that energy costs could ease on the potential reopening of the Strait of Hormuz.

Fixed Income: The 10-Year Treasury yield pulled back to end the week at 4.47% on geopolitical optimism. The Fed will convene on June 16-17 for Kevin Warsh’s first meeting as Fed Chair. There is virtually no expectation for a rate increase or decrease, but investors will be listening closely for insight into the new Chair’s thoughts on the Fed’s next move.

Commodities: West Texas Intermediate crude oil futures fell sharply on renewed hopes for peace in Iran. WTI closed out the week below $86.50 per barrel, the lowest level since early March, while Brent crude ended at $87.44. Over the weekend, news that Iran had agreed to sign the US Memorandum of Understanding put further pressure on crude prices and pushed WTI to below $81. Gold prices continued to fall, attributed to increased expectations for higher interest rates. Gold ended the week around $4,200 per ounce.

WEEKLY ECONOMIC SUMMARY

Consumer Price Index: The May Consumer Price Index rose 0.5% to an annual rate of 4.2%, showing accelerating inflation but in line with expectations. The Core rate (excluding food and energy) was more moderate at 0.2%, up 2.9% annually, which provided some hope to investors that energy costs are not yet having a significant impact on broader prices. Gasoline prices are up 40.5% year-on-year, and Fuel Oil has increased 58.9%.

Producer Price Index: May data on wholesale prices was less encouraging than the CPI released the day prior. PPI inflation was much higher than expected, coming in at 1.1% for the month to bring the annual rate up to 6.5%. Ex-food, energy, and trade core PPI was up 0.8% in the month and 5.1% year-on-year. The fact that core PPI was also hot contradicted the CPI data that showed price increases largely concentrated to energy costs. PPI is considered a leading indicator of CPI, so consumers could see rising prices in the coming months.

Iran Update: The week started off with increased hostilities after an Iranian drone was able to down a US Apache helicopter, prompting retaliatory strikes on Iranian military sites and a water reservoir. The rhetoric quickly shifted, however, after President Trump announced he was holding off from further strikes due to progress in peace negotiations. The US submitted a peace proposal to Iran that is still under review. Israel issued a formal statement clarifying that they are not party to the Memorandum of Understanding, which may be a sticking point as Israel and Iran-backed Hezbollah forces in Lebanon continued hostilities over the weekend.

The week ahead: The mid-week Fed meeting and press conference will be the main event during a holiday-shortened week with markets closed on Friday for the Juneteenth holiday.

CHART OF THE DAY

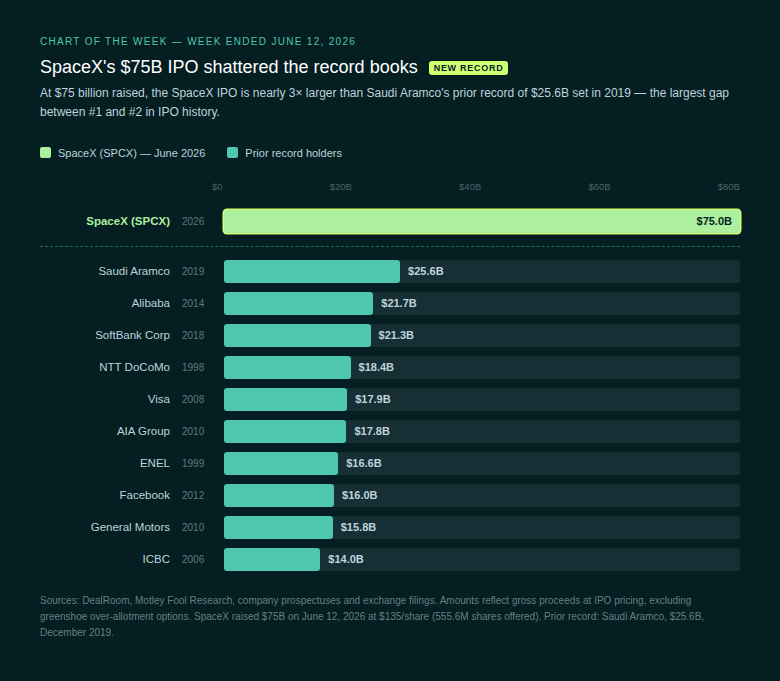

The Chart of the Day illustrates the unprecedented size of this week’s SpaceX (SPCX) IPO, in which 555.6 million shares were offered at a fixed opening price of $135 each, raising $75 billion. While the $75 billion offering is nearly three times the prior largest dollar-amount (Saudi Aramco in 2019), the total shares sold in the IPO represent only roughly 5% of SpaceX’s total outstanding equity. The remaining 95% of the company remains locked up by existing shareholders, including Elon Musk, who retains a 46% ownership stake. SpaceX ended its first day of trading up roughly 19.5% at $161.27, giving the company a valuation of more than $2.11 trillion, making it the seventh largest company in the world by market capitalization. The strong retail demand for the SpaceX IPO bodes well for other high-profile offerings expected this year, namely Anthropic and Open AI.

Chart and commentary by VestGen Investment Management.