WEEKLY MARKET SUMMARY

Global Equities: Stocks pulled off a second consecutive week of gains in a holiday-shortened week despite a negative mid-week reaction post-FOMC meeting. Semiconductor stocks gave a lift to the major domestic indices and led to outperformance for the Nasdaq Composite, which advanced 2.4%. The S&P 500 ended the weekly session up 0.9% while the Dow Jones Industrial Average closed 0.7% higher. Small cap stocks maintained recent momentum despite odds of a rate hike shifting forward to September, climbing 1.2% during the week. Foreign Developed stocks lagged on US dollar strength, pulling back -0.6%, while emerging markets benefited from semiconductor demand and outperformed with a 4.3% weekly jump.

Fixed Income: Treasury markets were little changed during the week, despite heavy attention on bond markets as Kevin Warsh assumed leadership as new Chairman of the Fed. A more hawkish FOMC triggered the stock market’s worst “Fed Day” reaction under a new Chair since 1994, but the 10-Year ended the week relatively steady at 4.49% after a brief foray above the 4.5% level.

Commodities: Progress towards peace in Iran ahead of the weekend’s anticipated formal implementation of the Memorandum of Understanding pulled oil prices sharply lower, culminating in a 10% weekly pullback in US West Texas Intermediate crude to under $77 a barrel. Gold prices continued to slide on dollar strength and rising rate-hike odds, falling to around $4,170 per ounce.

WEEKLY ECONOMIC SUMMARY

Retail Sales: May Retail Sales rose 0.9% month-over-month, nearly double consensus expectations, and were up 6.9% year-over-year. Higher gasoline prices boosted receipts at the pump, but spending held up broadly across categories; a core measure stripping out the most volatile categories rose 0.7%, reinforcing the view that consumer spending remains resilient even with elevated fuel costs and inflation. It is important to note that Retail Sales are not inflation-adjusted, and most of the rise is due to higher prices and not higher levels of consumption.

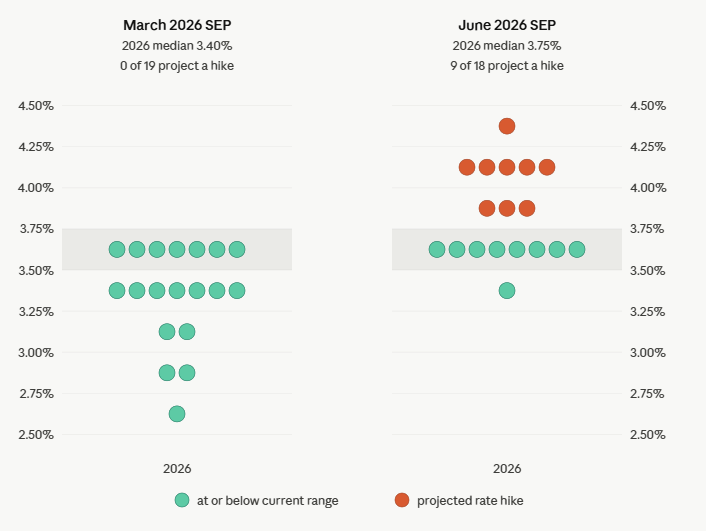

Fed Meeting: Kevin Warsh’s first FOMC meeting resulted in unchanged rates, as anticipated, but a hawkish shift in outlook, among other changes. The median “Dot Plot” forecast moved from projecting cuts to hikes, while the new Chairman refrained from offering his own personal forecast. Warsh has expressed a desire for several reforms to the Fed, which he outlined in his press conference. Among the changes is a reduction in the forecasting and communications the central bank provides, which was evident in a dramatically shorter FOMC statement. Warsh also announced the formation of several “task forces” at the Fed, aimed at improving communications and data accuracy.

Iran Update: The U.S. and Iran signed a memorandum of understanding establishing a 60-day window to negotiate a lasting peace deal and reopen the Strait of Hormuz, initially sending oil prices sharply lower. However, the agreement faced a highly volatile start as formal negotiations began in Switzerland over the weekend. Following public threats from President Trump to resume military strikes, the Iranian delegation briefly walked out of the venue, and Tehran abruptly announced it had re-closed the Strait of Hormuz. While Qatari and Pakistani mediators successfully pushed negotiators into an overnight session to establish a 60-day roadmap, the truce remains extremely fragile. Unresolved issues, including Israel’s vow to maintain military operations in southern Lebanon and Iran’s nuclear program, continue to inject uncertainty into the markets.

The week ahead: The Fed’s preferred inflation benchmark, the Core Personal Consumption Expenditures (PCE) index, will be released on Thursday, along with Durable Goods data and the final estimate of first quarter GDP.

CHART OF THE DAY

The Chart of the Day shows the upward shift towards a year-end rate hike from the Federal Reserve, illustrated by examining the change in the “Dot Plot” Summary of Economic Projections from March to June. At the March FOMC, the median projected rate for 2026 stood at 3.40%, with all 19 participating FOMC members expecting rates to remain at or below the current range. However, by the June 2026 meeting, the median projection climbed to 3.75%, driven by a significant split in consensus where 9 out of 18 participants revised their outlook upward to project a rate hike (with Chairman Warsh declining to provide his view). Inflation is the driving force behind the hawkish change, and until the Iran war is resolved, it appears the Fed simply cannot justify a cut.

Data: US Federal Reserve. Chart and commentary by VestGen Investment Management.